Recession Management: Strategies in the Staffing Industry

by Timothy B. Faber

We are well into one of the longer recoveries in U.S. history. It’s no surprise that there are talks of an impending slow down. When will it happen? How severe? How long will it last? What will be the trigger? In particular, how will it affect the Staffing Industry? What are the key strategies required to navigate a recession?… and as importantly, how to come out the “other side” in a stronger, more competitive position. Drawn from practical and industry experience, here are some approaches proven successful at managing in and through a recession.

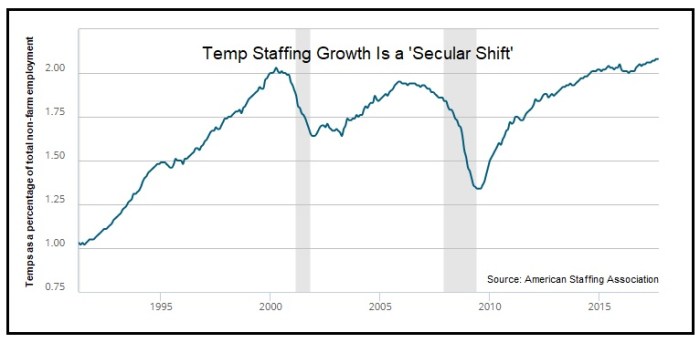

As with many sectors, the Staffing industry is not immune to recession and economic downturns. During the most recent recession – the Great Recession – declines were as great as 30% depending on the industry segment and geographic areas evaluated; however, as with all past recessions, the industry rebounded to a level well exceeding its’ past performance [see Chart 1].

A Primer of Industry Behavior

The industry tends to be an economic indicator1, leading trends by three to six months ahead of the overall economy. Businesses will often slow hiring or begin layoffs as the economy softens and demand for products and services decline.

Generally, the use of permanent or executive recruiters is affected first and by the greatest measure as companies eliminate this expense or bring the function in-house. Temporary help or staff augmentation (the largest sector of the staffing industry) demand tails-off more slowly and in fact may temporarily increase as companies shift to a flexible workforce rather than permanent staffing levels.

Regardless, these declines tend to happen prior to an economic slowdown, and for some, the industry has become a bellwether of hiring trends, labor absorption, and general economic health.

For many industries, the use of temporary help supplements a consistent, permanent level of staffing – essentially using staffing as the variable component. As headcount levels drop, it is not uncommon for temporary staff usage to drop before layoffs begin at the corporate employee level.

Conversely, as the economy begins to recover and product and service demands increase, companies prefer to increase their contingent staff usage rather than committing to increasing expensive headcount. Therefore, the industry typically shows signs of an impending recovery ahead of improvements in GDP or employment trends.

As noted, the industry has experienced exceptional growth the past ten years and, as customary, continues to expand to new levels following each recession. This expansion is a result of several factors:

- Increasing penetration of temporary workers relative to total employment – February 2018 setting a new record of 2.04%

- Expansion of services well beyond typical commercial services to include IT, healthcare, professional, etc. – services offered are expanding

- Continued education of target customers on the economic advantages offered by staff augmentation and a flexible workforce – the customer base is expanding

- The continued acceptance – and indeed a trend – of the gig/freelance workforce

It is important in a discussion of managing a staffing firm during a recession, that we are cognizant to expansion opportunities during the recovery. Failure to be prepared – which is required posturing during a downturn – will result in a failure to capitalize on post-recession opportunities.

Approaches

Managing through a recession – particularly in the staffing industry – is similar to many other sectors in that implementing an effective cost containment plan early in the cycle is important to maintaining and guarding profitability.

With that said, it’s vital to mitigate financial risk if you believe a downturn is looming without removing an aggressive posture towards growth. In other words, a viable and proven strategy is to maintain an investment in low-cost growth initiatives and posture to avoid being “hung-out” with irreversible, heavy investments, i.e. capital expenditures with long paybacks.

Invest in Low-Cost Sales Efforts

As a practical example, a typical (lower cost) growth initiative is to ensure all branches and business units are adequately staffed with operations and sales personnel to not only maintain current levels of business, but to provide capacity and bandwidth for growth. Interestingly, this is one of the least expensive growth initiatives and perhaps the least risky…excess headcount can be lowered quickly dictated by economic cycles and as needed.

Avoid Long Payback Investments

More expensive, long-term initiatives, such as opening new offices, can be throttled back as we begin seeing signs of weakness.

A typical new branch office carries a $200,000 budget to cover opening expenses, losses incurred before reaching breakeven, and cash flow for accounts receivables and working capital.

Most branches reach breakeven in six months with an acceptable level of contribution margin in a year. “Good” contribution margin typically arrives in the eighteen to twenty-four month range. Understanding this investment, and the eventual lag of profitability, leads us to slow the velocity of office openings as we begin to feel demand softening. Effectively, we want to avoid over-extending with large, quasi-fixed investments as a recession approaches.

Other Considerations

Obviously there are other cost-containment efforts as part of an established plan – reduction in corporate overhead, a review of all receivables (accelerating if possible), an “under the microscope” review of all expenses to include purchasing power opportunities, compensation changes, spending moratoriums, etc.

While a plan is critical and needed (in fact we should always have a cost containment plan in process), the key to getting through a recession and enjoying the frothy recovery afterwards, is a function of sales.

Sales it Is

In the 90-91’ recession, we were able to maintain the velocity of new clients we enjoyed prior to the recession. How? By increasing our sales & marketing activities…and, in fact, adding headcount to our marketing and sales teams.

At first this may seem counter-intuitive, but, the dynamics of a recession offer, and even dictate, unique sales and client acquisition opportunities. Admittedly, this initiative is a function of and regulated by the environment, however, what better time to invest heavily in sales as when your competitors are choosing to reduce their efforts?

A Practical

Looking at one group of competitors in particular, it becomes evident that an aggressive marketing approach is needed.

The industry is comprised of independents, franchises, regional, and national companies. Franchises as an example, typically pay 30-40% of their gross margin to the franchisor as a fee. This payment along with other shared fees or expenses (advertising funds) reduce GM%s by as much as 50% depending on related pricing factors. All things being equal, franchises (which are a fairly large percentage of staffing offices in the U.S.), as a competitive population, are half as profitable as independent offices.

For comparison, the breakeven of a typical independent branch is approximately 1200 billable hours per week. For a franchise with the burden of a franchisee fee, breakeven approaches 2500 billable hours – they have to do twice as much business volume for the same level of GM.

Thus, during a recession, the franchise owner will begin reducing office headcount and marketing investments much sooner than the independent. While this is intuitive, there is another layer of operating intelligence to consider…they typically begin that headcount reduction with sales staff and marketing representatives – protecting the operations core staff as a last measure of defense.

Though unfortunate, this provides an interesting sales opportunity.

Looked at on a broad scope, many franchises, and in some cases independent and corporate competitors, will begin reducing sales staff. As a result, clients may not see or have communication with competitors for extended periods of time.

In severe cases (similar to the Great Recession where the downturn lasts for years), many smaller firms and franchise operations are unable to weather the storm…they simply neither have the financial resources for an extended trough nor anything left to cut (expenses) – therefore closing their businesses…offering yet another competitive opportunity.

More eye-popping than just the sheer numbers is how fast freelance work is growing. Since 2014, the first year the survey was conducted, the number of freelancers has grown 8.1%. The American workforce during that time increased 2.6%. At the current rate of growth, the survey predicts the majority of workers will do some freelancing by 2027. – John Zappe – TLNT.com

And while franchises are particularly sensitive to swings in revenue, independents and larger firms are as well. Many staffing companies have relied on long-term relationships and large, low margin accounts – leaving marketing and sales to opportunistic and referral account gains. For privately held, lifestyle businesses, it’s hard to argue with any strategy that is successful. However, recessionary periods reduce revenue and put downward pressure on margins as competitors grapple for business.

For those unprepared, staff is lost to layoffs, accounts are lost and offices closed. This has a cleansing affect for those not prepared on the balance sheet or those that are marginal or under-achievers from a customer service or sales perspective.

Thus, the outcome of sales staff cuts is many clients lose their established staffing relationship – either at the individual representative level or the branch/location relationship. Assuming the client continues to need staff augmentation services (though albeit at lower levels), there is no one to turn to…except for those who have continued to invest in sales and marketing efforts.

As empirical evidence, we boosted sales efforts (in fact, added salespeople) during the previous recession and enjoyed a volume of new client acquisitions equal to pre-recession levels. Additionally, many of the sales staff released by competitors were available and on the market – free of non-competes. An added bonus – we were able to choose among excellent people who brought with them established client relationships.

Though this strategy may sound like a panacea, many of these efforts are rewarded with the win of not losing business volume and revenue. Practically, all clients reduce hiring and the use of temporaries during a recession. The increase or stabilized volume of new client flow is happily accepted as keeping revenue flat – often a win during any recession.

What happens on the other side?

The net effect of high or stable client acquisition during a recession often equals explosive growth during a recovery.

During periods following the 1991 recession, in particular in 1993-1995, revenue growth was exponential as a result of this strategy. While new client acquisition continued at an even or increased pace, existing clients were rapidly ramping up hires and investing in contingent staffing – wary of their recent bruising.

Concurrently, competitors who had reduced staff – operations, recruiting, and sales – were just beginning spinning-up headcount. Clients who had been lost during the downturn, were gone for good. Excellent staff that had been laid-off had found new homes and were direct competitors. Offices that had been closed, were re-opened only to find themselves in a new competitive landscape and facing possible years of effort to return to profitability.

“We are in the Fourth Industrial Revolution — a period of rapid change in work driven by increasing automation, but we have a unique opportunity to guide the future of work and freelancers will play more of a key role than people realize” – Stephane Kasriel, CEO of Upwork – https://www.upwork.com/press/2017/10/17/freelancing-in-america-2017/

Technology as a catapult

All retractions force us to look inward and evaluate processes, costs, technologies, applications, as well as staffing levels throughout the organization.

In 1991 there simply was little we could do in terms of accelerating or improving our efficiencies with technology…those technologies simply did not exist…yet.

The staffing industry is at the earliest phases of adopting automation technology, but the learning curve is quick. Onboarding is a logical place to start, as many of the tasks are standardized. We expect to see a dramatic increase in the quality and quantity of tools available in the marketplace for every stage in the next few years. Matt Fischer, President and Chief Technology Officer, Bullhorn

During the 2007-2010 recession, technology had ample time to progress. The period during and immediately after the recession new technologies were introduced that could only be enabled by high-speed communications, massive expansion of bandwidth, mobile applications, and remote app access via the “cloud”.

The result? For those companies who were wise to the investment of technology they are probably enjoying improved efficiencies.

“The workforce is experiencing changes as never before, with economic transformation driven by new technologies and automation” – Sara Horowitz, founder and executive director of Freelancers Union.

For instance, in the early 90’s a typical branch office was staffed with four people to maintain 2400 billable hours – management, operations/recruiting and sales. That staffing level allowed for adequate coverage for the business volume and allowed for excess growth and continued marketing. While that number hasn’t necessarily changed, the requirement to have that many people has become more flexible – due primarily to increases in productivity via technology.

Effective Strategies

A vigilant cost containment program combined with an aggressive sales and marketing program works very well. New accounts acquired during a slowdown often blossom during a recovery. Clients who have struggled and with whom you have a close relationship or have partnered in staffing efforts, appreciate the loyalty and assistance during rough times. Competitors who are recovering have a long and steep road ahead to re-establish themselves, and they are hampered with the reality that many of the industries best people have landed with those firms who have taken an aggressive tactic during the recession.

Small business owners are showing unprecedented confidence in the economy as the optimism index continues at record high numbers, rising to 107.6 in February, according to the NFIB Small Business Economic Trends Survey, released today. The historically high numbers include a jump in small business owners increasing capital outlays and raising compensation.

As an observation, consider this example in the Atlanta metro area. Randstad, whose North American headquarters is in Atlanta, launched a full-push radio campaign just as there were signs the recession in 2009-2011 was at its trough. Most competitors were continuing to reduce staff and marketing dollars. While we’re not privy to the outcome of that campaign, I suspect that most prospective clients viewed Randstad top-of-mind and the campaign exhibited strength in the local staffing sector. As more of a presumption, I argue they gained significant market share, as well.

M&A Opportunities

From an M&A perspective, post-recession opportunities have typically been excellent both in volume of firms available and quality of earnings, operations and staff, pricing, and lower valuation multiples.

For companies that weathered the downturn, they often are more lean and efficient, and generally have postured operations and sales for a long duration recovery. The more fortunate companies have invested in sales and marketing and are beginning to experience that investment – but, it hasn’t quite materialized. So, as with so many sectors, those using acquisitions as part of the corporate strategy, find post-recessionary periods producing a diverse population of target opportunities.

Outlook

It is not new news that we have been in an extended recovery as of this writing Q1 2018. However, we could argue that the recovery (though technical for several years) is just picking-up in small small to mid-sized businesses. The NFIB (National Federation of Independent Businesses) most recently (see charts below) indicates the recovery has finally caught-up with smaller firms.

This is excellent news for staffing companies as smaller firms comprise the bulk of diverse, non-concentrated revenue.

Also, unemployment is hovering at all-time lows in several geographies of the U.S. putting constraints on hiring via a tight labor market – posing the challenge (and opportunity) of using recruiting as a competitive advantage.

An estimation of how long this recovery will last is outside the scope of this paper, however, we do know a 2.5% GDP tends to absorb available talent at a reasonable rate.

GDP growth exceeding this level typically kicks-in wage increases (wage inflation) which drifts into consumer prices for goods and services, which drifts into capital costs and costs of goods, resulting in a slowdown or possible recession triggered by inflation (and rising interest rates). The Federal Reserve has announced interest rate increases which, in part, are intended to keep growth in check – mitigating inflation and over-baking the economy.

Summary

While a recession is inevitable, it presents a unique opportunity. For investments where an exit is planned or desired, a recession may elongate that exit yet offer expansion, EBITDA, and revenue opportunities that are not available during periods of economic expansion.

Summarily, managing through a recession may be reduced to several primary initiatives. All have been executed in the past and have been shown successful to varying degrees. And while a downturn is rarely an enjoyable event, there are tactics that can provide a successful transition or bridge while positioning for opportunities in the recovery.

- Guard against the long-term spend – don’t over-extend

- Invest in low-risk, low-cost sales efforts such as expanding an office/clerical office into light industrial staffing

- Leverage technology for efficiencies

- All expenses under the microscope – planned cost containment

- Make opportunistic acquisitions – companies, branches & accounts

Copyright 2018-2024, Talant Staffing

1 Harris Nesbitt The Staffing Indicator – January 2016 – “While temp staffing may not be a leading economic indicator, it appears that changes in temporary staffing at least suggest directional changes in total US employment. A 1995 study by the Federal Reserve Board of Chicago showed that changes in temporary staffing employment “lead” changes in aggregate US employment by roughly four to six months (using trailing 15-month averages for SIC 7360, the “old” BLS code for the personnel supply services sector).”